Where Data Intelligence Changes the Equation

The vendors who consistently outperform in this market share one characteristic: they know considerably more about their target utilities than those utilities might expect. They’re judiciously tracking utilities, mapping the full stakeholder network strategically and skillfully aligning to specific capital plans, compliance pressures, and funding cycles. None of it is a shot in the dark and that comes for them being aware that none of it can afford to be.

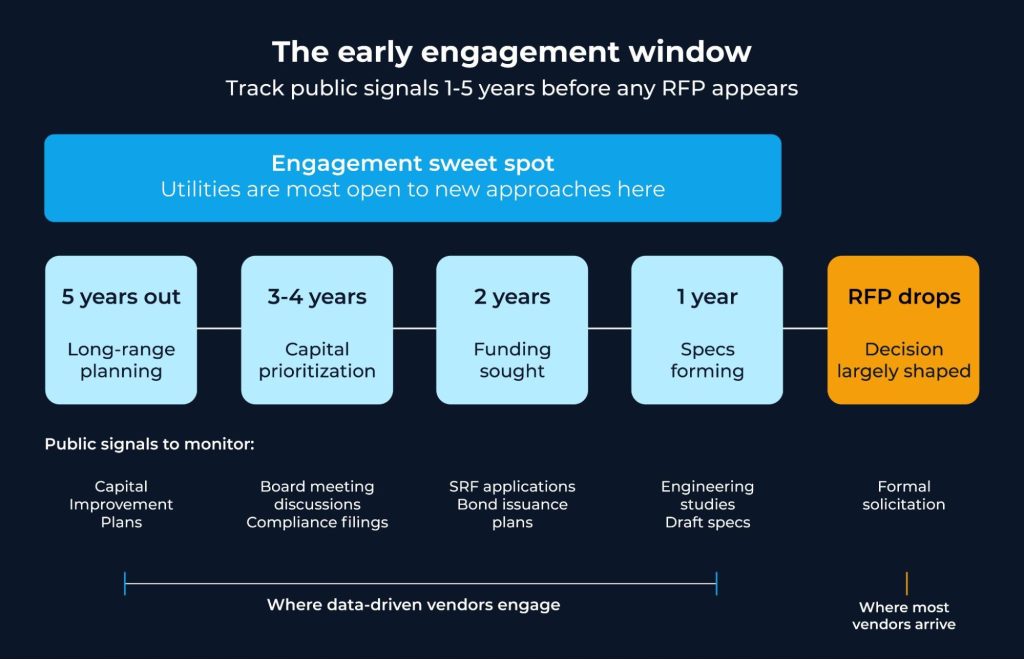

Modern data intelligence platforms are making this process a lot more systematic. Rather than waiting for procurement signals, they assist in monitoring thousands of public information sources to surface projects 1-5 years before any RFP appears. This is done by analysing:

- Capital Improvement Plans

- State Revolving Fund applications and awards

- Board meeting discussions about infrastructure needs

- Compliance challenges that will drive future investment

Early visibility enables relationship-building during the formative stages when utilities are the most welcoming towards new approaches.

The advantage shows up long before procurement does:

Beyond project identification, the more sophisticated platforms build comprehensive utility profiles with asset inventories, financial analyses, operational data, regulatory compliance status. The picture this creates matters because of a problem that’s not highlighted as much or is likely to be underestimated:

According to data from Trinnex:

- 90% of utilities cannot easily access their own data, trapped in disconnected IT systems, spreadsheets, or paper records

- 45% report that this directly limits their ability to manage operations and maintenance

The vendors who arrive with genuine insight into a utility’s operational picture can add tangible and purposeful input from the very first conversation; long before any formal proposal is written.

Decision influence mapping takes the stakeholder problem seriously in a way that most current approaches don’t. Advanced analytics can identify the full network of stakeholders influencing procurement:

- Organisational structures and reporting relationships

- Individual roles in previous project approvals

- Committee memberships and voting patterns

- External relationships with engineering firms and consultants

Getting this right means that the majority of the messages that were sent out reached all relevant decision influencers, with content tailored to their specific concerns. And that tailoring matters more than most vendors realise, because every interaction demands for a curated topic to focus on that is relevant and most importantly, desirable. If there isn’t a need to work towards and after, it is all ultimately to vain. Tailored value articulation follows naturally from having that context:

- Operations staff: reliability, maintenance requirements, staffing implications

- Finance departments: lifecycle costs, energy efficiency, grant eligibility

- Utility leadership: regulatory compliance, public perception, long-term planning

- Elected officials: rate impacts, environmental benefits, community outcomes

On the funding side, sophisticated platforms track not just the existence of funding sources but also their cycles involving SRF priority systems, federal grant deadlines, bond issuance plans, and whether specific projects have been secured versus prospective funding. Something to note is that proposals synchronised with actual funding availability convert at meaningfully higher rates than those that aren’t.

A McKinsey analysis has noted that generative AI and related technologies have the potential to automate work that currently absorbs 60-70% of employees’ time; this is a finding with real implications for the water utility sales process, where the manual work of tracking plans, mapping stakeholders, and aligning to funding cycles is exactly the kind of structured information problem that data platforms can handle efficiently.

Ashwin Dhanasekar of Brown and Caldwell has characterised the broader challenge plainly: aging infrastructure, escalating operational costs, and persistent data silos, all pressing simultaneously. The vendors who understand that specific combination for a specific utility earn a fundamentally different kind of conversation.

As S&P Global’s Veronica Retamales Burford has noted, physical risks, including water stress will increasingly drive investment decisions across industries, generating sustained regulatory and capital activity in this sector for years ahead. While Begoña Tarrazona of Idrica has observed, digital solutions will drive the transformation needed to optimize resources, enhance environmental sustainability, and improve efficiency in water-intensive applications.

The intelligence gap between vendors who know, vendors who guess and vendors who put matters to ‘snooze’ is widening. The platforms are widely accessible and so is the data. The only question is who’s using it.

What This Means in Practice

For vendors serious about improving their performance in this market, a few shifts make a material difference:

- Assess your current intelligence honestly: how and when you’re actually identifying opportunities, and how much of the decision has already been made by the time you engage.

- Extend your horizon: shift focus toward projects 1-5 years into the planning stage, when utilities are most open to new approaches and specifications haven’t been written yet.

- Build real utility profiles: asset base, capital plans, regulatory pressures, financial structure, and the relationships between the people who shape major decisions.

- Get serious about funding: if you cannot talk authoritatively about SRF cycles, WIFIA mechanisms, or how a utility balances rate implications and grant qualification, you will be missing out on crucial conversations.

- Map the full influence network: identify all stakeholders involved in purchasing decisions, their priorities, and how they relate to each other.

- Evaluate your process honestly: you must assess tactically whether your current method of opportunity assessment and qualification can handle all the above, or if you are merely relying on a combination of manual record-keeping and individual relationships.

The water utility market possesses a space for every vendor who strives to do better and put in the work. The infrastructure need is real, the capital is moving, and the gap between what vendors currently know and what’s actually knowable about their target utilities is wide. Closing the data disconnect might seem like a marginal operational improvement but it’s the very difference between competing ruthlessly and actually securing a deal.