America’s water infrastructure is aging rapidly and only the vendors who know how to spot the warning signs early are securing contracts.

There are 2.2 million miles of drinking water pipes in the country, and their average age is over 45 years. Wastewater lines? About 800,000 miles of them, with 30% already past 50 years old. Treatment plants are running equipment that’s been in the ground since the 1970s.

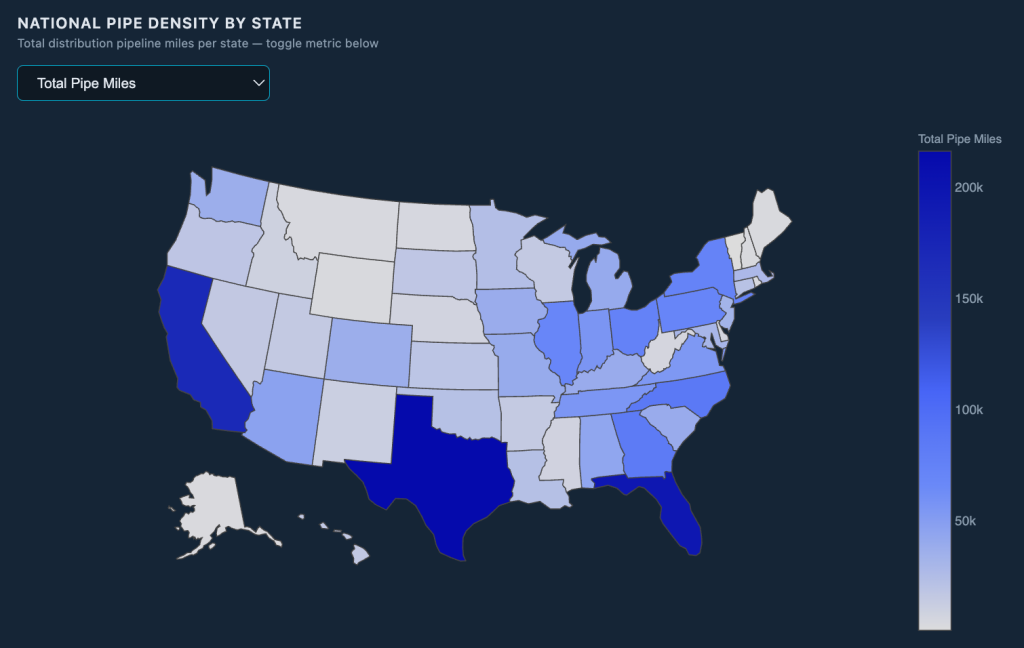

Fig 1: Depicting National Pipe Density by State: Total Pipe Miles

As illustrated in Figure 1, total pipe mileage is heavily concentrated in a handful of states, with the South and West carrying a disproportionate share of the country’s distribution infrastructure. Much of this represents decades of accumulated investment that is now well into its ageing cycle.

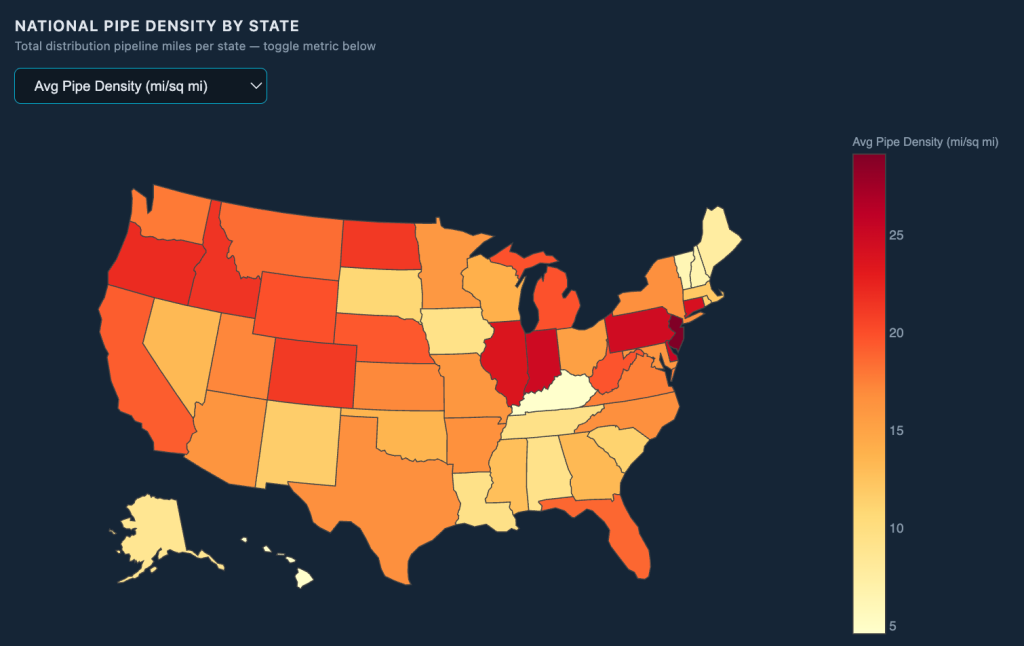

Fig 2: Depicting National Pipe Density by State: Average Pipe Density

When measured against land area, the Northeast and parts of the Midwest emerge as the most pipe-dense regions in the country. More infrastructure packed into less space means tighter interdependencies, less redundancy, and considerably less margin for failure as these networks age. (As shown in Figure 2)

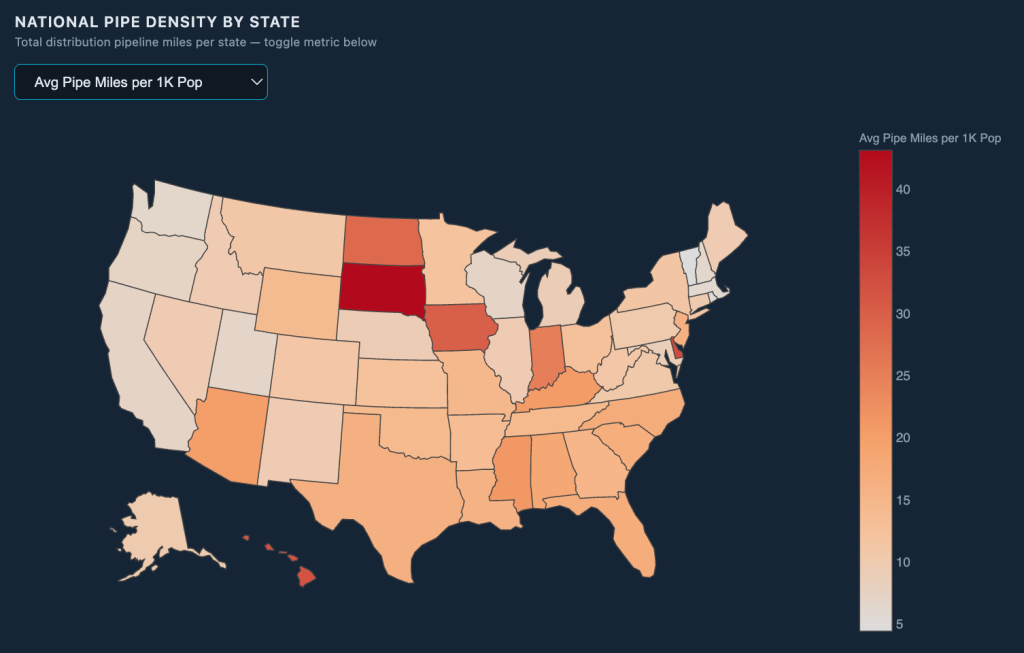

Fig 3: Average Pipe Miles per 1K Pop

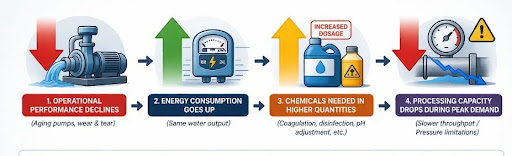

What happens when infrastructure gets that old? It inevitably fails.

According to a report from a Utah State University & American Society of Civil Engineers, water main breaks cost utilities $2.6 billion per year to repair. Nearly 20% of U.S. water pipes (about 452,000 miles)as highlighted in this U.S. water utility market overview are past their useful life and need replacement. Yet funding to fix it is nowhere near adequate. The EPA says there’s a $309 billion funding gap right now, and by 2043, that number balloons to $620 billion.

For water utilities, this is a crisis. For equipment manufacturers, engineering firms, and service providers, it’s an opportunity, but only if they know how to capitalise on it.

Figure 3 surfaces a dimension of this crisis that gets the least attention. Across much of the rural interior, pipe infrastructure per capita is the highest in the country. These regions are served by smaller utilities, thinner budgets, and the same ageing problem as everywhere else, with far fewer resources to deal with it.

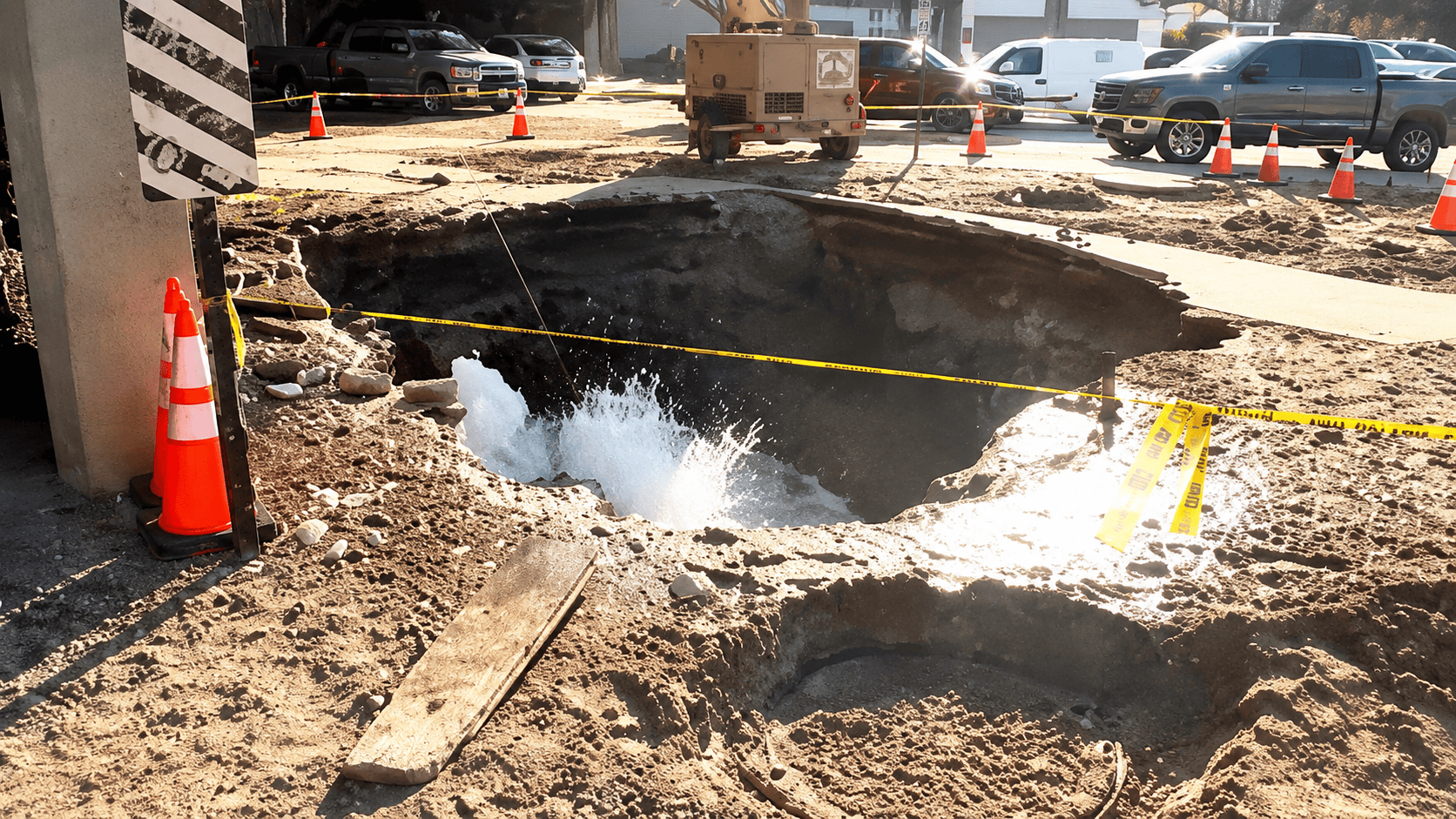

Water main break caused by aging water infrastructure is a growing challenge for water utilities across the United States.

The Vendor Disadvantage

Most vendors approach this the traditional way. They respond to RFPs when utilities finally put out formal requests and by that point, they’re already behind.

By the time an RFP appears, the utility has already defined what it requires and multiple competitors have started circling around it. Pricing pressure is brutal and the vendor’s chance to shape the solution is gone, who then becomes a bidder fighting on p

rice instead of a trusted advisor shaping the solution.

That’s the reactive approach, and it doesn’t work anymore.

The Predictive Advantage: Getting There First Changes Everything

Organisations that identify equipment replacement needs before utilities do experience dramatically different results. Research shows vendors who spot need 12+ months early achieve:

- 3.4x higher win rates on the opportunities they pursue. Not slightly better: 3.4 times better.

- 28% larger average contract values. They’re not competing on price; they’re designing solutions that address actual needs.

- 40% shorter sales cycles once procurement actually starts. Early relationships compress timelines.

- 67% less competitive pressure. They’re not battling three other vendors for the same contract.

The difference is massive. A vendor that gets in early, shapes the conversation. They position themselves as a trusted advisor, not a supplier. They influence specifications before they’re set and build relationships with multiple stakeholders before the RFP stage. By the time formal procurement happens, the utility already knows who they want to work with.

How Equipment Actually Gets Replaced: It’s Rarely a Sudden Decision

Here’s what most vendors don’t understand: Equipment replacement doesn’t happen overnight. Utilities don’t turn up one day and decide to replace a 40-year-old pump. It’s a gradual process that unfolds over months, sometimes even years, leaving signals along the way.

Maintenance costs start climbing. A pump that costs $5,000 to fix annually suddenly needs $12,000 in repairs and it isn’t long before it spikes to $18,000. At some point, usually when annual maintenance exceeds 15-20% of the replacement cost, someone in the utility starts asking, “Should we just replace this thing instead?”

As infrastructure ages, the cost dynamics between routine operations, inspections, and reactive repairs begin to shift. Over time, the cumulative cost of continued repair can approach or exceed the cost of planned replacement.

These aren’t things utilities want to advertise, but they show up in operational reports, regulatory submissions, and board meeting discussions.

Regulatory requirements changeunder laws like the America’s Water Infrastructure Act. These cause for a new permit to come up for renewal with stricter limits. The utility’s existing equipment can’t meet the new standards, and just like that, replacement isn’t optional: it’s mandatory. These regulatory transitions happen on predictable timelines.

Budget allocations shift as projects begin to get funded, water utility capital improvement plans get updated, engineering study funds appear and rate studies begin, after which bond offerings are discussed. These are signals that money is available and projects are moving forward.

From here, engineering work begins, utility commissions, condition assessments and feasibility studies get started. They reach out to consulting engineers and explore alternatives. This preliminary work happens months, sometimes years, before any formal procurement.

A vendor who understands these signals and monitors for them can engage utilities at exactly the right moment. Not too early, when utilities aren’t thinking about replacement yet. Not too late, when specs are already written out which is where installed base replacement intelligence becomes critical.. Right in that window where the utility is recognizing a problem and starting to explore solutions.

What This Means Going Forward

The aging infrastructure crisis isn’t stopping. If anything, it’s accelerating. Utilities know what’s coming. They know pipes are failing and that treatment plants need upgrades, but they’re resource-constrained and often don’t know where to start.

Vendors who can help utilities identify what needs fixing and when, who can come in as trusted advisors rather than salespeople, who can shape solutions instead of just bidding on them, those vendors win. They win bigger contracts and build relationships that last. The window to capitalise on this is open now. The infrastructure is aging. Funding is available through programs like the EPA Clean Water State Revolving Fund.. Utilities are ready to act. The vendors who understand this and build systems to identify needs early and engage appropriately, will dominate the next five years in water infrastructure.